555-555-5555

mymail@mailservice.com

The Gender Gap in Banking: Challenges and Solutions for Pakistan

Imagine a Pakistan where every woman has control over her finances. Now, compare that vision to today’s reality: only 13% of women in Pakistan have access to financial accounts, while 34% of men do. It’s not just a gap it’s a chasm, reflecting decades of systemic inequality.

According to the World Bank’s Global Findex 2021, 21% of adults in Pakistan are financially included, leaving us far behind the global average of 69%. This exclusion isn’t just a statistic; it’s a barrier to progress, innovation, and empowerment—particularly for women.

What’s standing in the way of a more inclusive financial system? And more importantly, how can we make a change?

The future of Pakistan’s economy depends on these answers. Let’s explore them together.

The Cost of Exclusion: Challenges for the Banking Sector

Missed Market Opportunities

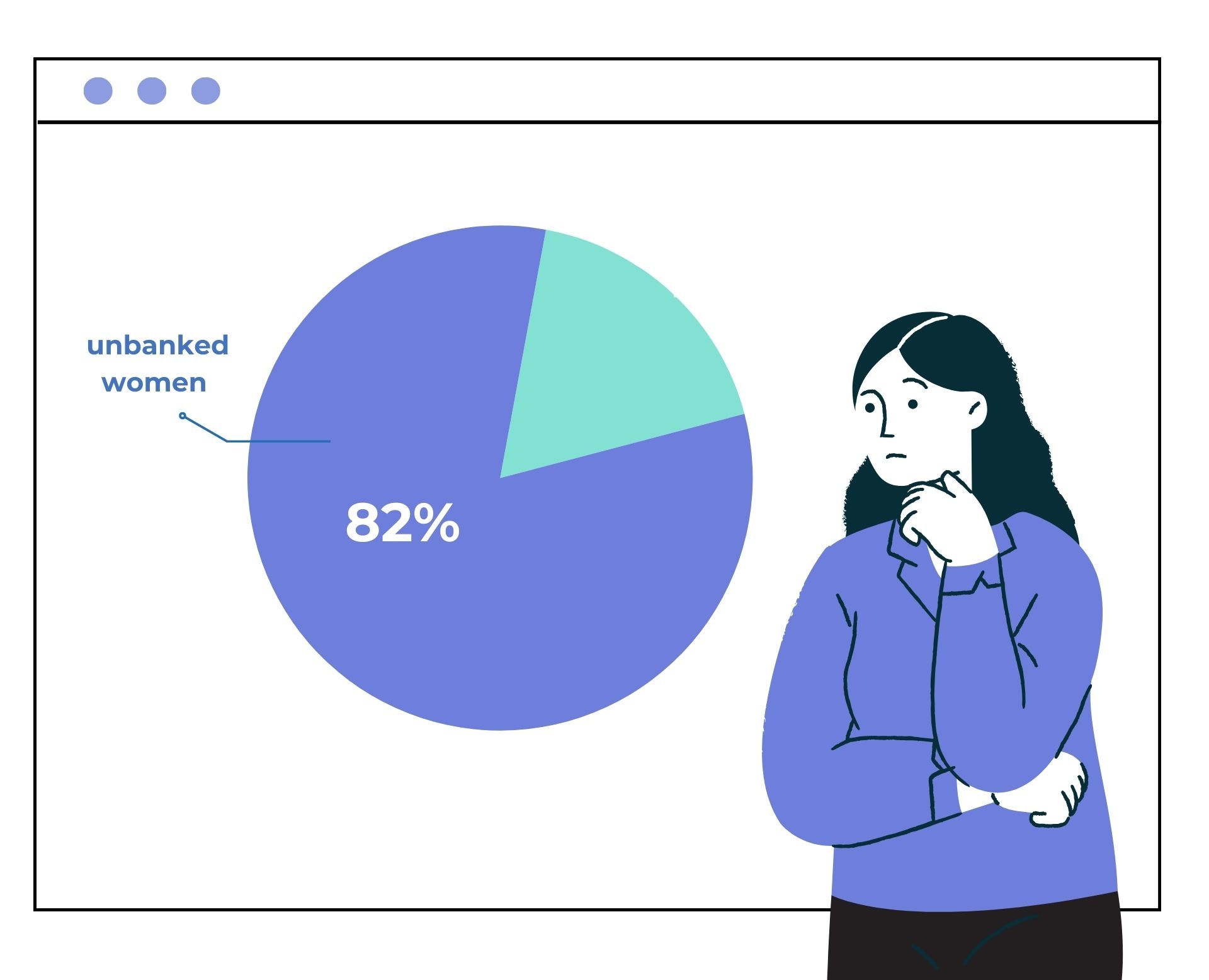

Women make up a vast, untapped customer base. With 82% of Pakistani women unbanked, financial institutions are missing out on a market worth over PKR 101 billion ($650 million) annually. This isn’t just about inclusion it’s about generating a revenue stream that could significantly boost the banking industry. Women represent a largely untapped market for financial institutions.

By failing to address the unique needs of this segment, banks are overlooking a significant opportunity for growth. Beyond the numbers, this points to a deeper disconnect between traditional banking models and the realities of fostering an inclusive economy.

Reduced Customer Diversity

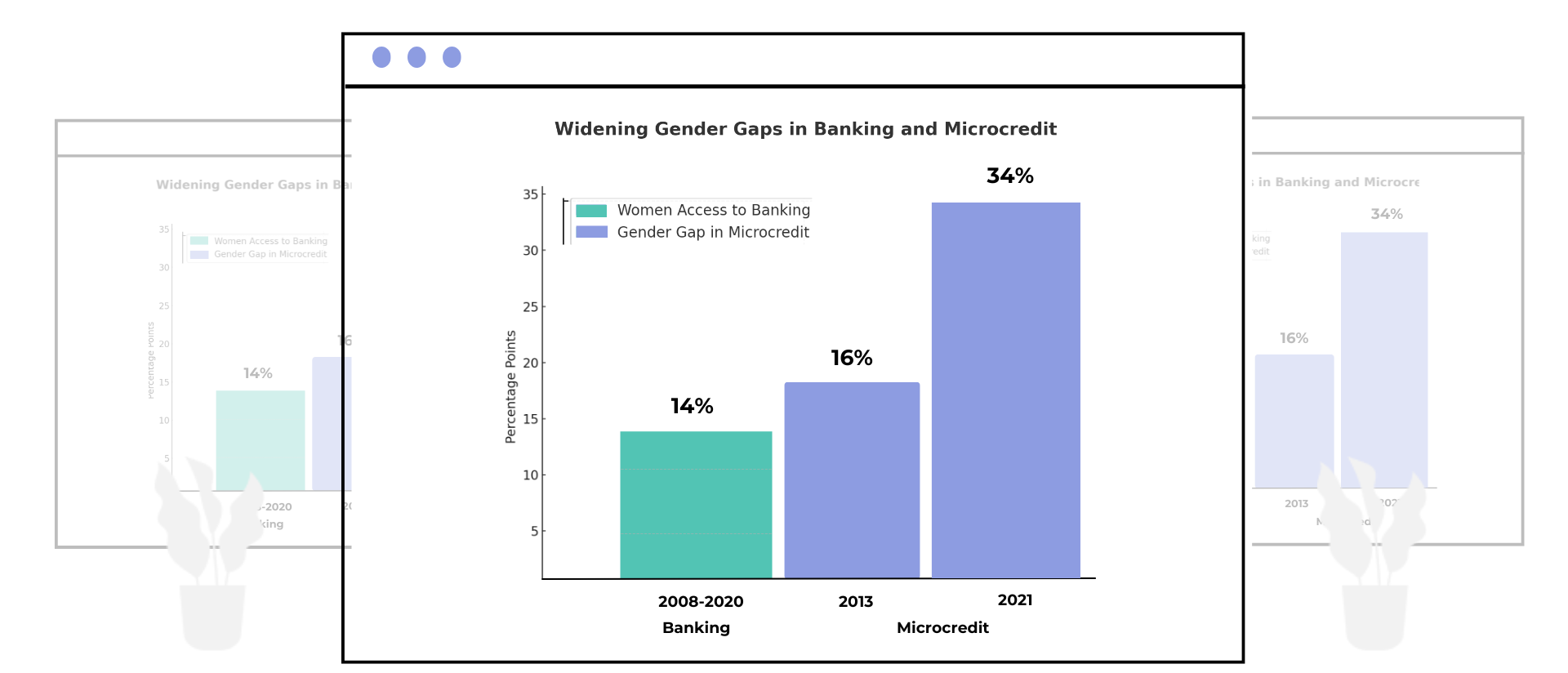

From 2008 to 2020, while women’s access to banking improved by 14 percentage points, the gender gap actually widened, favoring men disproportionately. Similarly, microfinance disparities have deepened, with the gender gap in microcredit distribution growing from 16% in 2013 to 34% in 2021. This lack of diversity not only limits growth but also reinforces societal inequalities.

Operational and Growth Limitations

The exclusion of women hinders banks from fully utilizing their branch networks and digital platforms.

Expanding services to underserved areas, particularly rural regions, remains a challenge due to cultural and logistical barriers.

Missed Competitive

Edge

As global markets embrace gender-focused financial strategies, Pakistan risks falling behind. Women entrepreneurs who make up 22.63% of the workforce remain underrepresented in professional and managerial roles,

with only 7.4% in STEM fields. This untapped potential could drive innovation and growth if addressed effectively.

Excluding women from the financial system doesn’t just limit their opportunities—it restricts the banking sector’s potential to innovate and compete globally. Women bring diverse perspectives and behaviors that could revolutionize traditional banking practices if banks embraced their inclusion fully.

Reputational Risks

The financial sector’s gender-neutral policies have often proven inadequate in addressing inherent gender inequalities. Recognizing this, the State Bank of Pakistan (SBP) has mandated that banks achieve 20% female representation in their workforce by December 2024. Institutions failing to comply risk reputational damage and regulatory penalties.

Closing the Gap: How Banks Can Respond

To bridge this divide, banks must adopt innovative, inclusive, and practical approaches.

Financial Literacy Programs

Knowledge is empowerment. Women need to understand how financial systems work to make informed decisions.

Example: HBL Nisa combines workshops with women-focused financial products to enhance financial literacy.

Impact: Builds confidence and encourages proactive financial engagement.

Women entrepreneurs often face barriers to securing loans. Flexible credit terms and reduced collateral requirements can help.

Example: The First Women Bank Limited (FWBL) provides dedicated credit and savings products exclusively for women.

Impact: Empowers women to grow businesses and contribute to the economy.

Tailored Financial Products

Women need financial products that align with their unique circumstances.

Example: The UBL Urooj Account offers minimal balance requirements and exclusive benefits like shopping discounts.

Impact: Encourages women to save and invest, fostering long-term financial security.

Financial products designed for women are not just about lower balances or perks—they’re about acknowledging and addressing the unique challenges women face. Products like these can empower women to take charge of their finances and build confidence in managing money.

Digital Banking Solutions

Digital platforms can overcome mobility and cultural barriers, providing women with easier access to financial services.

Example: Easypaisa, in collaboration with NGOs like Karandaaz, has successfully onboarded rural women into digital payment systems.

Impact: Enables greater inclusion through mobile wallets and simplified transactions.

Digital solutions hold the key to breaking long-standing barriers to inclusion. By integrating digital tools with cultural sensitivities, banks can redefine access and create a user-friendly gateway to financial independence for women.

Gender-Inclusive Policies

Increasing representation in the workforce and leadership is crucial for creating an inclusive banking environment.

Example: The SBP’s Banking on Equality Policy mandates a 20% female workforce in banks by 2024.

Impact: Encourages a culture of inclusivity and diversity.

The Benefits of Inclusion: Why It Matters for Banks

Market

Expansion

According to the World Bank, including just 10% more women in the financial system could generate over $1 billion in annual revenue.

Revenue

Growth

Women are consistent savers. For example,

HBL Nisa has driven a 10% increase in savings deposits.

Reduced Loan Default Risks

Women borrowers often exhibit higher repayment rates, making them a safer bet for banks.

Regulatory Compliance and ESG Alignment

Gender-inclusive policies enhance Environmental, Social, and Governance (ESG) scores, attracting foreign investment and strengthening reputational standing.

Empowering women financially isn’t just beneficial for individual banks—it creates a ripple effect across the economy. Inclusive banking fosters a sense of trust, engagement, and progress that ultimately benefits everyone, not just women.

Lessons from BRAC Bank: A Model for Success

Bangladesh’s BRAC Bank has shown what’s possible with a focused approach.

Its TARA program offers tailored financial products for women, contributing to a 15% growth in deposits and expanding women’s share of the customer base to 18%.

Relevance for Pakistan: Pakistani banks can replicate such initiatives to tap into underserved female markets.

Moving Forward: A Shared Responsibility

Bridging the gender gap in banking isn’t just about empowering women—it’s about driving economic growth and societal equity. By developing innovative products, leveraging digital solutions, and fostering inclusivity, banks can transform challenges into opportunities.

It’s time to close the gap. What steps do you think can drive financial inclusion for women in Pakistan? Let’s continue the conversation share your thoughts below!

Need Help?

🏠︎ Dolmen Executive Towers, Level 7

Clifton Block 4, Karachi, Pakistan

Postal Code 75600

Site Links

Recent Blog Posts