555-555-5555

mymail@mailservice.com

Financial Literacy for All: Empowering Low-Income Families to Use Banking Services

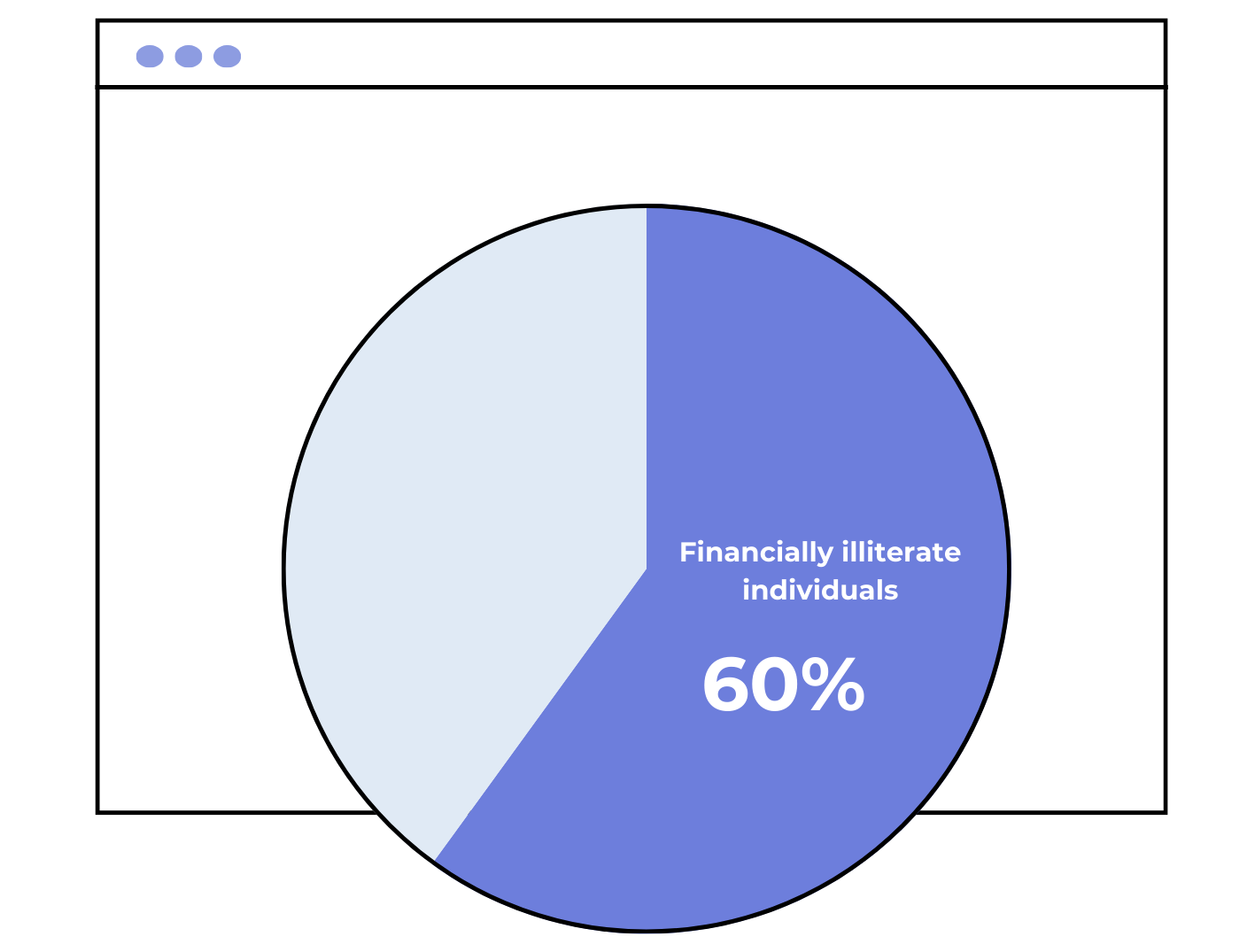

Did you know that 73% of financially literate individuals feel more confident about their future, while 60% of those without financial literacy struggle to plan ahead? These findings from a PwC survey underscore a harsh reality—financial knowledge isn’t just about money; it’s about security, stability, and peace of mind.

With a general literacy rate of around 62% in 2024, Pakistan still faces an even more alarming challenge—financial literacy. Despite being able to read and write, millions lack the financial knowledge needed to secure their future.

Financial literacy rates in the country remain critically low, hovering between a mere 19% to 25%. As a result, millions, especially low-income families, are left navigating a complex financial world without the right tools. This lack of awareness prevents them from using banking services effectively, saving for the future, and breaking free from cycles of economic hardship. But the impact goes beyond their wallets—financial stress is now closely linked to rising mental health issues across the country, as inflation and economic pressures take a toll on individuals and families alike.

Change starts with knowledge. When financial literacy reaches everyone—especially those in underserved communities—it paves the way for growth, stability, and a brighter future. Imagine the possibilities when low-income families have the right tools to take charge of their finances and shape their own success. It’s time to make that happen.

The Impact of Low Financial Literacy on Individuals in Pakistan

Financial literacy is more than just understanding money—it's the key to making informed decisions that shape an individual's financial future. In Pakistan, where financial literacy rates remain critically low, a large segment of the population struggles with fundamental financial tasks, leading to long-term economic challenges. From poor financial decisions to increased vulnerability to fraud, the consequences of low financial literacy can be severe.

Let’s explore the major impacts and how they affect individuals in Pakistan, backed by insights and data.

Poor Financial Decision-Making

Lack of financial knowledge often results in individuals struggling with budgeting, saving, and investing. Poor financial decision-making can lead to excessive debt, insufficient savings, and an inability to build financial security. A study indicates

that in Pakistan, financial literacy tends to improve with age and experience rather than through formal education

(SSRN). This insight indicates that many young individuals enter adulthood without the necessary skills to make sound financial choices, which can have long-term consequences on their economic well-being.

Limited Access to Financial Services

When individuals lack an understanding of financial products and services, they are less likely to utilize formal banking options, restricting their economic participation.

According to

PAFEC, only 13% of Pakistanis have formal bank accounts placing the country 16th among 26 nations with the lowest financial literacy levels.

This underutilization of financial services keeps many individuals dependent on informal financial systems, limiting their access to credit, secure savings, and investment opportunities, which are essential for financial growth and stability.

Increased Vulnerability to Financial Scams

Individuals with low financial literacy are more prone to falling victim to financial scams and predatory practices.

In Pakistan, the lack of awareness and understanding leaves people vulnerable to fraudulent schemes that exploit their limited knowledge (Usman Rasheed & Co). Many individuals unknowingly engage in high-risk financial dealings or invest in illegitimate schemes, ultimately facing significant financial losses. Increasing financial literacy is crucial to safeguarding individuals from such risks.

Limited Economic Empowerment

A financially illiterate population struggles to make informed economic decisions, ultimately impacting their ability to

achieve financial independence and empowerment.

According to ResearchGate, financial literacy programs play a vital role in enabling individuals to make informed choices that can improve their economic well-being.

In Pakistan, where financial education opportunities are scarce, empowering individuals through targeted financial literacy initiatives can bridge the knowledge gap and foster economic growth at both individual and national levels.

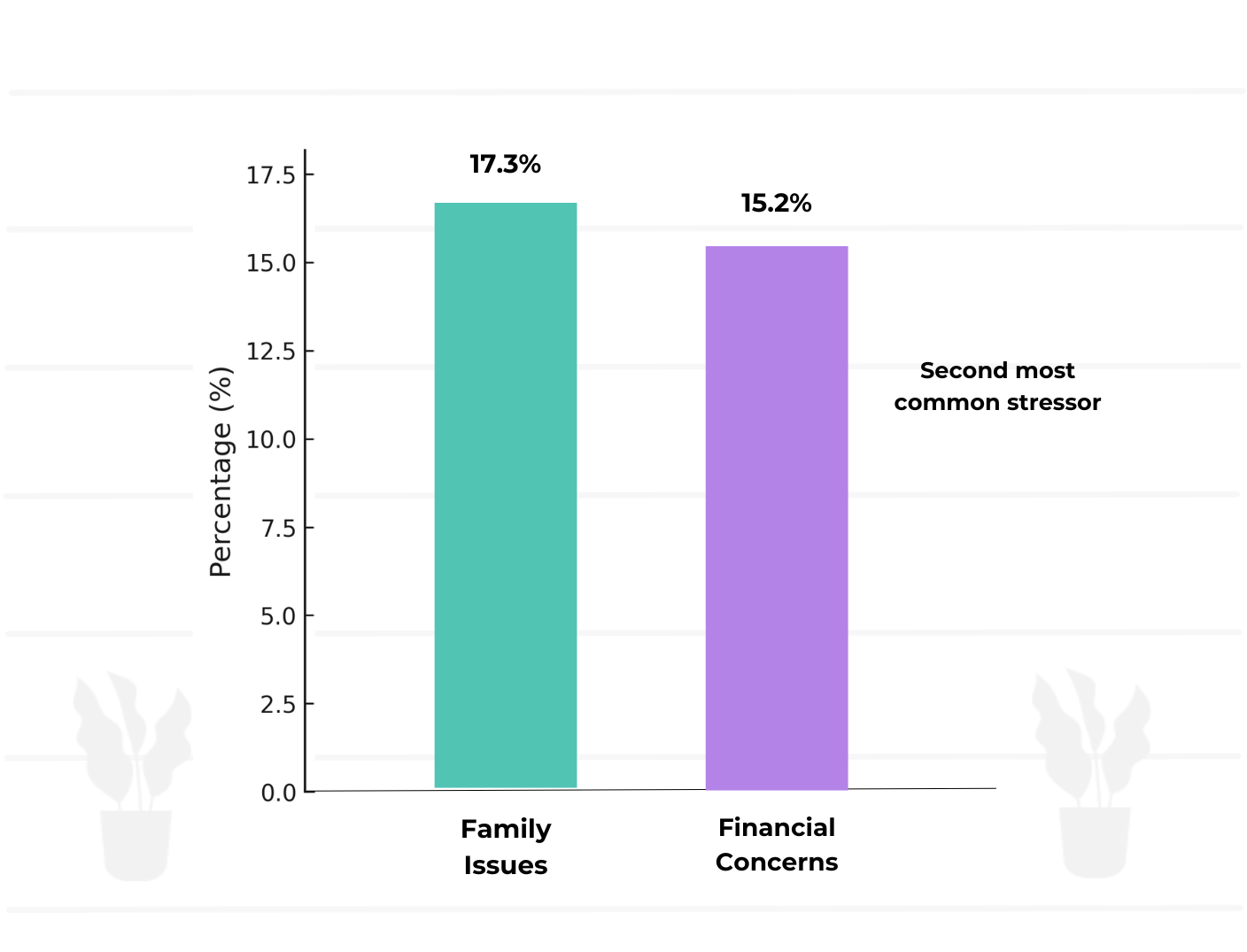

Higher Levels of Financial Stress

Mismanagement of personal finances, excessive debt, and lack of financial planning can lead to significant stress and anxiety. A survey conducted by Gallup Pakistan-

Pakistan's Foremost Research Lab

revealed that 17.3% of family issues are the leading cause of stress, while 15.2% of financial concerns rank as the second most common stressor.

Financial insecurity affects not only an individual’s mental well-being but also their productivity and overall quality of life. Enhancing financial literacy can provide individuals with the confidence and tools to manage their finances more effectively and reduce stress.

Inadequate Retirement Planning

Without adequate financial education, individuals often overlook the importance of long-term financial planning, resulting in financial insecurity during retirement.

In Pakistan, financial literacy is rarely included in school curricula, leaving students unprepared to handle personal finances effectively (Teen Ink). As a result, many individuals fail to plan for retirement, relying solely on family support or government assistance, which may not be sufficient to meet their needs in later years. Addressing this gap through financial education can help individuals build a more secure financial future.

Solutions to Improve Financial Literacy in Pakistan

To tackle financial literacy challenges, Pakistan needs a multi-pronged approach:

Integrating Financial Education in Schools

Introducing personal finance concepts early in school curricula will equip future generations with the tools to manage money effectively, fostering long-term financial stability.

Countries like Canada have shown the positive impact of financial education at a young age, leading to more financially responsible citizens. By adopting a similar approach, Pakistan can empower the next generation to build solid financial foundations early on.

Community-Based Financial Awareness Programs

Local financial literacy programs tailored to low-income communities can empower individuals with essential financial knowledge. Initiatives like India’s National Strategy for Financial Literacy have demonstrated that community-driven education can significantly improve financial understanding and behavior. By creating localized programs that address the unique challenges faced by Pakistani communities, we can ensure that education is accessible and relevant.

Promoting Digital Banking

Encouraging the use of

mobile banking services like JazzCash and Easypaisa can expand financial inclusion, making banking services more accessible, especially in rural areas. These platforms allow individuals to send money, make payments, and even save, all from the palm of their hand. By providing digital literacy alongside financial education, we can bridge the gap for those who lack access to traditional banking services.

Empowering

Women

Providing women with financial education and access to microfinance opportunities will enhance their economic independence and improve family and community well-being. Countries like Indonesia have seen significant improvements in household income through targeted programs for rural women. In Pakistan, similar initiatives could drive economic growth and create a more equitable society.

Leveraging Fintech Solutions

Fintech platforms, such as mobile wallets and digital payments, can bridge the accessibility gap, offering secure financial services to those without access to traditional banking. These platforms can help low-income individuals save, borrow, and invest without needing to rely on physical bank branches, bringing financial services directly to their fingertips.

Encouraging Insights from Around the World

Looking at global success stories can offer valuable lessons for Pakistan. Countries that have invested in financial literacy have seen improved economic resilience and financial well-being.

- Kenya's mobile banking revolution (M-Pesa) helped millions move out of poverty, demonstrating the power of accessible financial tools paired with literacy programs.

- Indonesia’s financial literacy programs for rural women increased household income by 25%, proving how targeted initiatives can create positive economic changes.

- Canada’s financial education initiatives successfully reduced personal bankruptcies, showing how well-structured programs can empower individuals.

These global examples provide valuable insights into the impact of financial literacy programs. By adapting these initiatives to Pakistan's context, we can overcome barriers and ensure that financial literacy reaches every corner of society.

The Road Ahead for Pakistan

Pakistan has the potential to transform its economic landscape by investing in financial literacy at all levels of society. From integrating financial education into school curricula to launching awareness programs for low-income groups, empowering individuals with financial knowledge can unlock a future of financial independence and growth. By drawing inspiration from global successes, Pakistan can foster a culture where every citizen has the tools to make informed financial decisions, leading to a more prosperous and secure nation.

Need Help?

🏠︎ Dolmen Executive Towers, Level 7

Clifton Block 4, Karachi, Pakistan

Postal Code 75600

Site Links

Recent Blog Posts